Comparing housing affordability in different African countries using purchasing power parity dollars

Comparing housing affordability in different African countries using purchasing power parity dollars

This blog was originally published in Janurary 2022, here: https://housingfinanceafrica.org/documents/an-explanation-of-the-approach-used-to-compare-housing-affordability-in-different-african-countries

A market price reflects the interplay between demand for the product concerned and its supply. The housing market is no different. Changes in the price of accommodation in a particular country can be due to any number of developments on either (or both) the demand or supply sides of the housing market. Tracking these prices using the currency of the country concerned is relatively easy, but the resulting trends can be distorted over time by a range of factors.

A market price reflects the interplay between demand for the product concerned and its supply. The housing market is no different. Changes in the price of accommodation in a particular country can be due to any number of developments on either (or both) the demand or supply sides of the housing market. Tracking these prices using the currency of the country concerned is relatively easy, but the resulting trends can be distorted over time by a range of factors.

For example, if the general price level in a country rises by 255% (as happened in Zimbabwe in 2019) then a similar increase in the price of accommodation would mean that in relative terms the cost of accommodation to households remained unchanged. If average household incomes rose by more than the inflation rate over the same period, then housing would actually be more affordable to most people – despite the significant increase in its price. If, however, the price of accommodation only increased by 200% over the same period and incomes rose by 150% then accommodation would simultaneously be relatively cheaper than most other items purchased by households, and less affordable relative to household income.

One way to reduce the potential distortions created by the passage of time is to eliminate the effects of inflation by deflating prevailing market values using the prices of a selected base year. Doing so makes it easier to examine volume trends and relative price changes.

However, the task of comparing housing affordability across different African countries is made more difficult because the cost of houses, and the incomes used to pay for them, are usually denominated in the local currency of the countries included in the analysis. For this reason, earlier editions of the Housing Finance in Africa Yearbook converted relevant elements of the affordability calculations into a single, internationally-accepted currency – the United States dollar – using prevailing market exchange rates. However, some countries have fixed or pegged official exchange rate systems that operate in conjunction with parallel or “black market” rates that often provide a more accurate reflection of economic fundamentals. For example, at the start of 2018, Angola had an official exchange rate of around Kz165/US$ and a parallel market rate of more than Kz400/US$. Those importers able to import at the official rate had a substantial advantage over those that had to use the parallel market.

In addition exchange rate movements are seldom consistent with inflation differentials and market exchange rates tend to be far more volatile over time than both house prices and incomes expressed in local currency terms. This is especially true of countries – of which there are a number of examples in Africa – with comparatively narrow export bases whose currencies are unduly affected by the prevailing prices of their primary export commodities on international markets.

Nigeria is a good example of this. Between May 2016 and May 2017, the Naira weakened against the US dollar by more than 58%, but over the same period inflation in Nigeria was around 16% while in the United States it was less than 2%. To reflect relative purchasing power, the Naira should only have weakened against the US dollar by around 14%. If house prices in Nigeria moved in tandem with consumer prices over this period they would have increased by 16.3% in local currency, but in US dollar terms they would have dropped by 27%. In the subsequent twelve months (May 2017 to May 2018), the Naira weakened by a further 14% against the US dollar while the inflation differential between the two countries dropped to just under 9%. In local currency terms, house prices would have increased by 11.6% if they matched CPI inflation, but in US dollar terms they would have dropped by a further 2%.

Because of the distortions that the use of prevailing market exchange rates can give rise to, the affordability calculations in the Housing Finance in Africa Yearbook for 2021 are converted into international purchasing power parity (PPP) dollars. A PPP dollar is a notional currency that reflects the rate at which the currency of one country would have to be converted into that of another country to buy the same amount of goods and services in each country. It takes account of the prevailing inflation rates in each country.

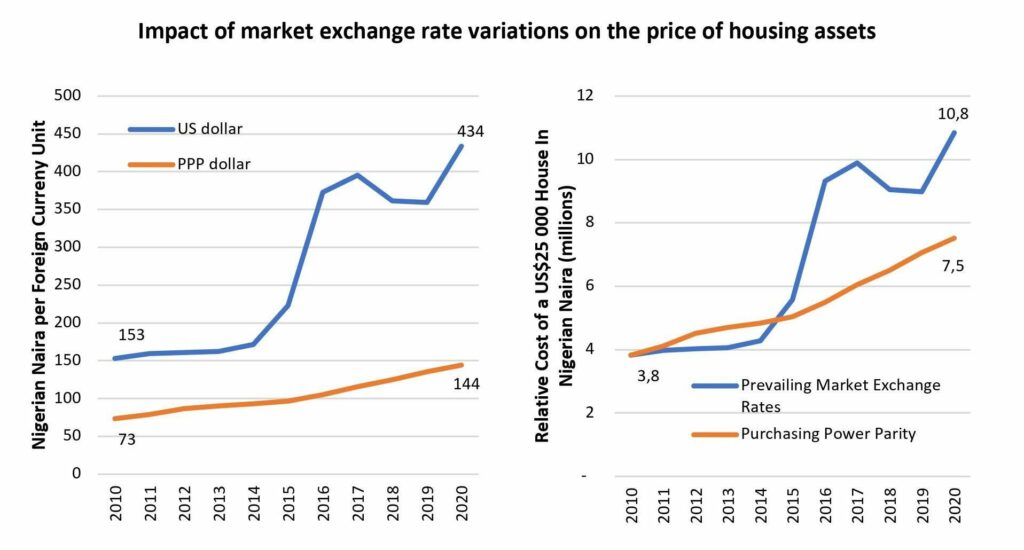

The figure below contrasts the relative movements in the exchange rate of the Nigerian Naira and the US dollar and the Naira and a PPP dollar (left-hand graph), with the impact of this variation on the price of an asset such as a house (right-hand graph). A house that cost US$25 000 (equating to NGN3.8 million at market exchange rates in 2010) would have cost around NGN10.8 million at prevailing market exchange rates in 2020. However, if the exchange rate had moved in line with inflation differentials (i.e. in line with purchasing power parity) the same house should only have cost NGN7.5 million.

The practical implication of this is that if the cost of producing a house in both countries changed in accordance with the inflation rates that prevailed in each country, you would have needed around 44% more Naira (converted at market exchange rates) to purchase an equivalent house (same type of neighbourhood, same size, same quality of finishes) in the United States than you would have needed in Nigeria in 2020. The prevailing market exchange rate undervalued the Naira by around 44% in 2020.

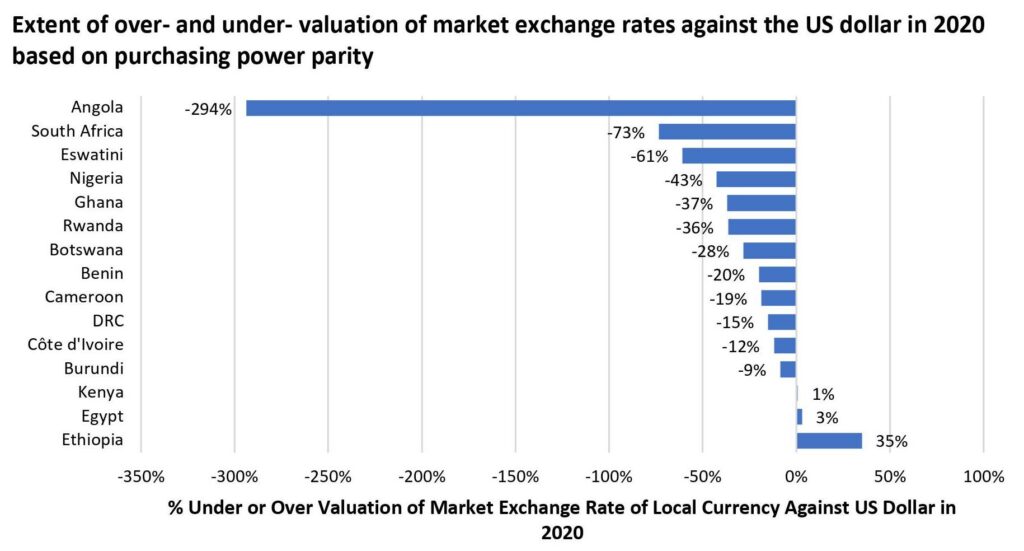

If the prevailing market exchange rates of different African countries were all undervalued to the same extent against the US dollar, it would still be possible to compare the relative cost of housing across countries with reasonable accuracy using the market-based exchange rates of local currencies to the US dollar. However, that is not the case – as the figure below shows. Relative movements in market and PPP exchange rates between 2010 and 2020 indicate that across a selection of African countries, the local currency generally depreciated against the US dollar by more than it should have – based on inflation differentials. The extent of this under-valuation in 2020 ranged from close to 300% in the case of Angola to 9% in Burundi. Three of the countries studied had local currencies that were over- valued in terms of their purchasing power in 2020. These were Kenya (1% over-valued), Egypt (3% over-valued) and Ethiopia (35% over-valued).

Comparing the costs of housing in different African countries using prevailing market exchange rates would therefore be distorted by the extent to which their local currencies were either under- or over-valued against the US dollar at that point in time. So if, for example, the price of a standard CAHF house in South Africa was compared with a standard CAHF house in Nigeria in 2020 using prevailing US dollar market exchange rates, the house in South Africa would be roughly 30% cheaper than the Nigerian equivalent based purely on the extent of the relative under-valuation of the two currencies.